笨狼发牢骚

发发牢骚,解解闷,消消愁

昨晚期待已久的日本央行再次降息没被采纳:

《彭博》Bank of Japan Stuns Market by Holding Off on More Stimulus

全世界到处都撒央行娇一般,大家于是叫苦连天,“The markets are saying the Japanese have to do more. They are already doing a ludicrous amount, but clearly it is not enough,” said Michael Every, an analyst with Rabobank International in Hong Kong. “Fiscal policy seems to be what we have to look at now”,一气之下一盘水泼过去:

(小时图)日经指数跳水过千点,说是把人民币都扯上了:

人民币被迫升值

《商业有线电视CNBC》采访

埃里安(Mohamed El-Erian,曾任太平洋投资管理公司(PIMCO)擔任首席執行官兼联合首席投资官老总)

“市场牵着央行鼻子走”

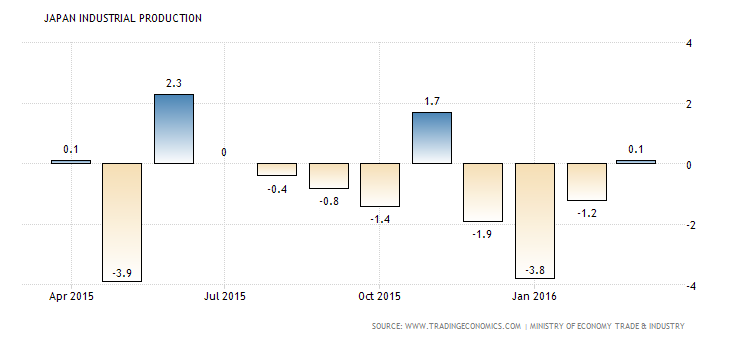

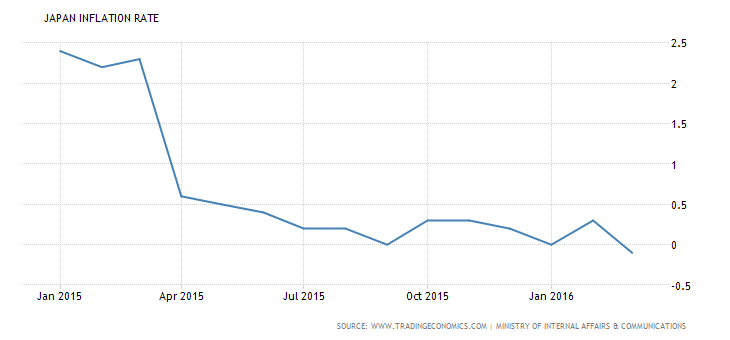

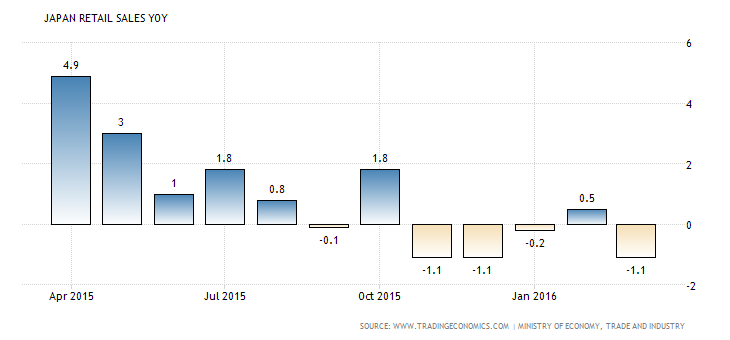

日本基本经济数据:

总产值

通胀率

零售量──走投无路的安倍政府不得不在明年加销售税,就像把百姓头上的刀子,大家提心吊胆

我说过多次,安倍黒田東彦的财政货币政策实在是毫无招数,日本只会每况愈下,慢慢消亡。

大家常常嘲笑黒田東彦时用的照片

一波未了,下波又来,今早美国公布今年一季总产值:

美国一季总产值增长率0.5%

鼓手们说:“别担心,咱一季度总是这样,冬天冷的”。去年冬天,那是热的了。我脑子常常困惑的是,既然经济总体指标这么糟糕,为什么就业那么强劲?那,可真是美国人自豪的。

失业人数十年来最低──抑或临时工人数最高?

春生夏长,好日子又来了。

【注】

《华尔街日报》戏称这是“Déjà Vu All Over Again”,故言“似曾相识鼠归来”。

【附录】

The Facebook Fallacy

For all its valuation, the social network is just another ad-supported site. Without an earth-changing idea, it will collapse and take down the Web

Michael Wolff May 22, 2012

Facebook not only is on course to go bust but will take the rest of the ad-supported Web with it.

Given its vast cash reserves and the glacial pace of business reckonings, this assertion will sound exaggerated. But that doesn’t mean it isn’t true.

At the heart of the Internet business is one of the great business fallacies of our time: that the Web, with all its targeting abilities, can be a more efficient, and hence more profitable, advertising medium than traditional media. Facebook, with its 900 million users, its valuation of around $60 billion (as of early June), and a business derived primarily from fairly traditional online advertising, is now at the heart of the heart of this fallacy.

The daily and stubborn reality for everybody building businesses on the strength of Web advertising is that the value of digital ads decreases every quarter, a consequence of their simultaneous ineffectiveness and efficiency. The nature of people’s behavior on the Web and of how they interact with advertising, as well as the character of those ads themselves and their inability to command attention, has meant a marked decline in advertising’s impact.

At the same time, network technology allows advertisers to more precisely locate and assemble audiences outside of branded channels. Instead of having to go to CNN for your audience, a generic CNN-like audience can be assembled outside CNN’s walls and without the CNN-brand markup. This has resulted in the now famous and cruelly accurate formulation that $10 of offline advertising becomes $1 online.

I don’t know anyone in the ad-supported Web business who isn’t engaged in a relentless, demoralizing, no-exit operation to realign costs with falling per-user revenues, or who isn’t manically inflating traffic to compensate for ever-lower per-user value.

Facebook has convinced large numbers of otherwise intelligent people that the magic of the medium will reinvent advertising in a heretofore unimaginably profitable way, or that the company will create something new that isn’t advertising, which will produce even more wonderful profits. But because its stock has been trading at about 40 times its expected earnings for the next year, these innovations will have to be something like alchemy to make the company worth its sticker price. For comparison, Google has been trading at a forward P/E ratio of around 11. (To gauge how much faith investors have that Google, Facebook, and other Web companies will extract value from their users, see this graphic.)

Facebook currently derives 82 percent of its revenue from advertising. Most of that is the desultory, ticky-tacky display advertising that litters the right side of people’s Facebook profiles. Some is a kind of social marketing: a user chooses to “like” a product, which is supposed to further social relationships with companies. The social network sells its ads by valuing various combinations of the cost of a thousand ad impressions (or CPM) and the cost of a click (CPC). Both forms of ads are more or less coarsely targeted to users on the basis of information they’ve volunteered to provide to Facebook and the sharing or “liking” of media within Facebook’s universe. General Motors recently announced it would no longer buy any kind of Facebook ad.

Facebook’s answer to its critics is: Pay no attention to the carping. Sure, grunt-like advertising produces the overwhelming portion of our $4 billion in revenues, and yes, on a per-user basis, these revenues are in decline. But this stuff is really not what we have in mind. Just wait.

It’s quite a juxtaposition of realities. On the one hand, Facebook is under the same relentless downward pressure as other Web-based media. The company’s revenue amounts to a pitiful $5 per customer per year, which puts it ahead of the Huffington Post but somewhat behind the New York Times’ digital business. (Here’s the heartbreaking truth about the difference between new media and old: even in the New York Times’ declining traditional business, a subscriber is still worth more than $1,000 a year.) Facebook’s business grows only on the unsustainable basis that it can add new customers at a faster rate than the price of advertising declines. It is peddling as fast as it can. And the present scenario gets much worse as people increasingly interact with the social service on mobile devices, because on a small screen it is vastly harder to sell ads and monetize users.

On the other hand, Facebook is, everyone has come to agree, profoundly different from the Web. First of all, it exerts a new level of hegemonic control over users’ experiences. And it has its vast scale: 900 million, soon a billion, eventually two billion people. (One of the problems with the logic of constant growth at this scale and speed is that eventually Facebook will run out of humans with computers or smart phones.) And then it is social. Facebook has, in some yet-to-be-defined way, redefined something. Relationships? Media? Communications? Communities? Something big, anyway.

The sweeping, basic, transformative, and simple way to connect buyer to seller and get out of the way eludes Facebook. It has to sell its audience like every humper on Madison Avenue.

The subtext—an overt subtext—of the popular account of Facebook is that the network has a proprietary claim to and special insight into social behavior. For enterprises and advertising agencies, it is therefore the bridge to new modes of human connection. Expressed so baldly, this account is hardly different from what was claimed for the companies most aggressively boosted during the dot-com boom. But there is, in fact, one company that created and harnessed a transformation in behavior and business: Google. Facebook could be, or in many people’s eyes should be, something similar. Lost in such analysis is the failure to describe the application that will drive revenues.

Google is an incredibly efficient system for placing ads. In a disintermediated advertising market, the company has turned itself into the last and ultimate middleman. On its own site, it controls the space where a buyer searches for a thing and where a seller hawks that thing (AdWords, its keywords advertising network). Google is also the cheapest, most efficient way to place ads anywhere else on the Web (through the AdSense network). It’s not a media company in any traditional sense; it’s a facilitator. It can eliminate the whole laborious, numbing process of selling advertising space: if a marketer wants to place an ad (that is, if it is already convinced it must advertise), the company calls Mr. Google.

And that’s Facebook’s hope, too: it wants to be a facilitator, the inevitable conduit at the center of the world’s commerce.

Facebook has the scale, the platform, and the brand to be the new Google. It lacks only the big idea. Right now, it doesn’t actually know how to embed its usefulness into world commerce (or even, really, what its usefulness is).

But Google didn’t have the big idea at its founding, either. The search engine borrowed the concept of AdWords from Yahoo’s Overture network (a lawsuit for patent infringement and a settlement followed). Now Google has all the money in the world to buy or license the ideas that could make its platform and brand pay off.

What might Facebook’s big idea look like? Well, it does have all this data. The company knows so much about so many people that its executives are sure the knowledge must have value (see our feature “What Facebook Knows”).

If you’re inside the Facebook galaxy—a constellation that includes an ever-expanding cloud of associated ventures—there is endless chatter about a near-utopian new medium for marketing. Round and round goes the conversation: “If we just … if only … when we will …” If, for instance, frequent-flier programs and travel destinations actually knew when you were thinking about planning a trip … If a marketer could identify the person who has the most influence on you … If an advertiser could introduce you to someone who would relay the advertising message … Get it? No ads, just friends! My God!

But so far the sweeping, basic, transformative, and simple way to connect buyer to seller and get out of the way eludes Facebook.

So the social network is left in the same position as all other media companies. Instead of being inevitable and unavoidable, it has to sell its audience like every humper on Madison Avenue.

But that’s what Facebook is doing: selling individual ads. If you consider only its revenue, it’s an ad-sales business, not a technology company. To meet expectations—the expectations that took it public at $100 billion—it has to sell at near hyperspeed.

The growth of its user base and its ever-swelling page views mean an almost infinite inventory to sell. But the expanding supply, together with equivocal demand, results in ever-lowering prices. The math is sickeningly inevitable. Absent that earthshaking idea, Facebook will look forward to slowing or declining growth in a tapped-out market, and ever-falling ad rates, both on the Web and (especially) in mobile applications. Facebook isn’t Google; it’s Yahoo or AOL.

Oh, yes … in its Herculean efforts to maintain its overall growth, Facebook will force the rest of the ad-driven Web to lower its prices, too. The low-level panic the owners of every mass-traffic website feel about the ever-downward movement of their CPM is turning to dread. Last quarter, some big sites observed as much as a 25 percent decrease, following Facebook’s own attempt to book more revenue.

You see where this is going. As Facebook gluts an already glutted market, the fallacy of the Web as a profitable ad medium will become hard to ignore. The crash will come. And Facebook—that putative transformer of worlds, which is, in reality, only an ad-driven site—will fall with everybody else.

Michael Wolff writes a column on media for the Guardian; is a contributing editor to Vanity Fair; founded Newser; and was, until October of last year, the editor of AdWeek.