笨狼发牢骚

发发牢骚,解解闷,消消愁

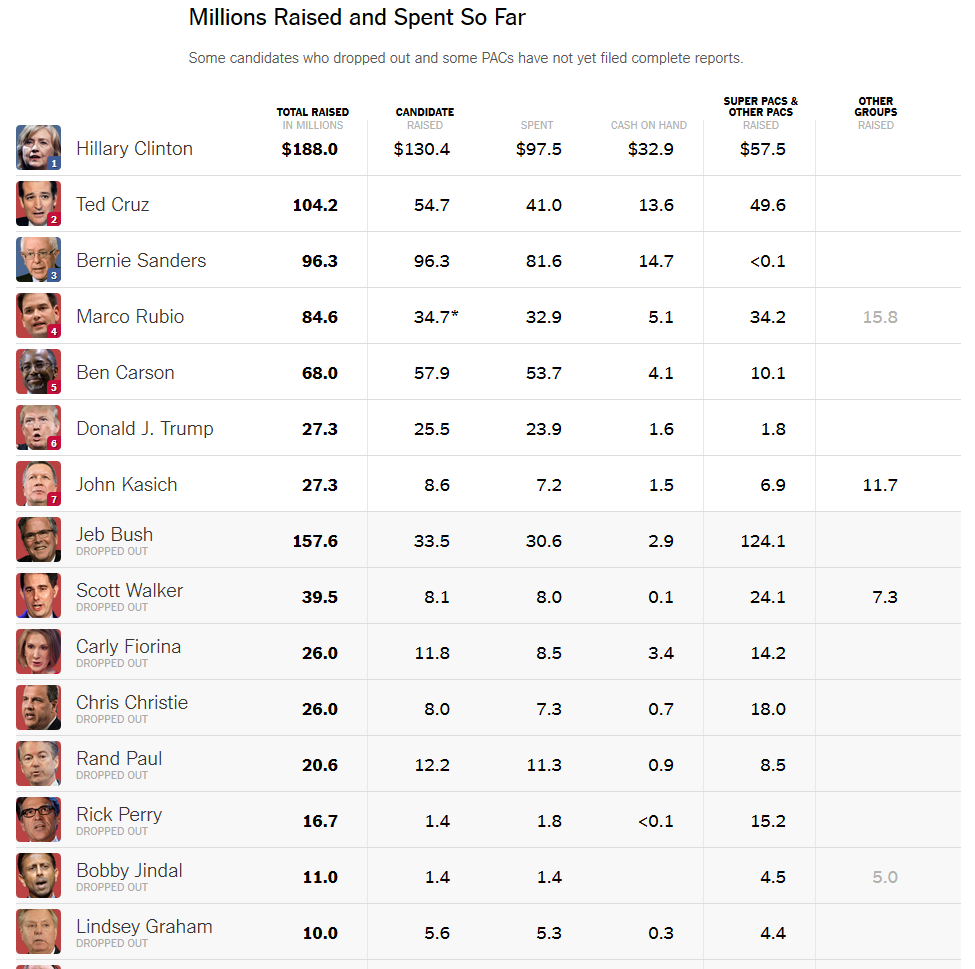

快一年了,记得彭博政坛老记者:明年美国大选上百亿。这是目前已经公布了的钱。

竞选好像很久了,但还是刚刚开始。据《纽约时报》总结,迄今参加美国总统竞选的人已经积聚了过十几亿美元,不过都是总统竞选。随着竞选日益变得激烈,只会有更多的钱涌进争斗。也许大家说闲得死和淳朴表明钱不是万能的,没钱一样办大事儿,我还是说总统就是钱买来的(彭博说买不来)。

【附录}

《纽约时报》

Uncovering the Bad Math (or Logic) of an Economic Analysis Embraced by Bernie Sanders

Justin Wolfers (Justin Wolfers is a professor of economics and public policy at the University of Michigan) FEB. 26, 2016

An academic study that predicted Bernie Sanders’s economic platform would cause an enormous economic boom turns out to have been based on faulty math, or bad economic logic.

The analysis produced by Professor Gerald Friedman, an economist at the University of Massachusetts at Amherst, got a lot of attention when it argued that fully implementing the Sanders program would lead per capita gross domestic product — a measure of average income — to grow one-third higher in 10 years’ time than it otherwise would be. In this economic nirvana, jobs would be plentiful, unemployment rare, poverty low, inequality less severe and the budget in surplus. The study is not an official campaign document, but it has been lavishly praised by Mr. Sanders’s campaign.

The Bernie Sanders campaign has lavishly praised an analysis that predicted Mr. Sanders’s economic platform would cause an enormous boom. Credit Sam Hodgson for The New York Times

The problem is that for all the name-calling, none of Mr. Friedman’s critics had figured out what he had gotten wrong.

Until now.

Christina Romer and David Romer, two of the leading macroeconomists of their generation and both professors at the University of California, Berkeley, have just released a careful forensic examination of Mr. Friedman’s analysis. (Ms. Romer was one of the four original Democratic economists who had criticized Mr. Friedman’s work. And full disclosure: Mr. Romer was for many years my collaborator in editing the Brookings Papers on Economic Activity.)

Their excavation uncovered one crucial but buried tidbit, and it’s basically the whole shebang.

But first, some background. Most economists believe that temporary increases in government spending will yield temporary increases in output. To see why the effect of stimulus is temporary, realize that if raising government spending raises output, then because the end of a stimulus program means cutting government spending, the same forces are later set in motion, but in reverse. And so in the standard story, a temporary stimulus improves the economy, but only temporarily.

Here’s the problem: Mr. Friedman’s calculations assume that removing a stimulus has no effect. The result is that temporary stimulus has a permanent effect.

The issue here is all about levels versus changes. In the usual telling, changes in government spending lead to changes in output. In Mr. Friedman’s spreadsheets, changes in government spending permanently raise the level of output. Mr. Friedman confirmed to me that this was how he had made his calculations.

The same levels-versus-changes confusion leads Mr. Friedman’s calculations to show that a permanent increase in the level of government spending — like that proposed by Senator Sanders — will yield a permanent rise in the rate of change of output. This is the reason he finds that the Sanders plan has such enormous effects on economic growth.

There are two interpretations of Mr. Friedman’s findings. The first is that he has simply gotten his math wrong. The second is that he has a different view about how the economy operates. Either way, his numbers don’t represent conventional economic thinking. And they’re at odds with empirical studies documenting that temporary fiscal stimulus does tend to have temporary effects.

Yet Mr. Friedman has described his analysis as “using standard assumptions and methods.” Likewise, his staunchest defender, James Galbraith, argued that, “What Professor Friedman did, was to use the standard impact assumptions and forecasting methods of the mainstream economists and institutions.” In copious footnotes, his paper quite self-consciously draws inspiration from standard analyses, such as those published by various government agencies.

The problem is that conventional analyses link changes in government spending to the changes in output, not to its long-term level as in Mr. Friedman’s analysis. Effectively Mr. Friedman is arguing that boosting government spending boosts the economy, but cutting government spending as the stimulus program ends has no effect. For all of the detail spelled out over 53 pages and 97 footnotes, this one critical assumption is never mentioned.

Here’s why this matters. Mr. Friedman claims to “make a conservative estimate of the stimulative effect of the Sanders program by using a relatively low spending multiplier.”

The multiplier is a number that quantifies how strongly government spending influences output. He relies on the Congressional Budget Office for estimates of the multiplier, and shades them a little, which makes them appear conservative. The multiplier he uses is on average 0.89. In the Congressional Budget Office models that he’s drawing from, this means that if the government spends $100 more today, output will rise by $89 this year, but when that stimulus is withdrawn next year, output will then fall back to its earlier level.

From start to finish, that $100 extra government spending yields $89 worth of more stuff. By contrast, in Mr. Friedman’s figures, output stays $89 higher each year, forever. Over a 10-year period, this means that $100 of government spending yields a total of $890 worth of more stuff, implying a 10-year multiplier of 8.9.

This is not a conservative estimate; it’s so high that I know of no study that suggests such large effects, nor of any economist who would defend this view. This is why Ms. and Mr. Romer say that Mr. Friedman’s “estimates of the likely demand effects are dramatically higher than standard approaches imply,” and that his estimates are “not just implausibly large, but literally incredible.”

When I pointed Mr. Friedman to this critique of his analysis, he simultaneously accepted and rejected it.

He accepted it, telling me that “I may have made a mistake.”

But he also rejected this critique, arguing that his figures are based on an alternative view of the world, stating: “To me, when the government spends money, stimulates the economy, hires people who spend, that stimulates more private investment. That remains, and at the next year, you’re starting at the higher level.” He admits that this “is not standard macro,” and described it as the understanding of an earlier generation of economists — a sub-tribe of Keynesians he called “Joan Robinson Keynesians.” (Joan Robinson was a contemporary of John Maynard Keynes at Cambridge.)

When I pressed Mr. Friedman on whether he was right to conclude that standard assumptions suggest that Mr. Sanders’s economic program will have such large effects, he said, “I have to stop saying ‘standard.’ ” It became apparent in our conversation that he simply hadn’t realized that he had mischaracterized mainstream economics, leading him to describe his disagreement with Ms. and Mr. Romer as “a measure of my ignorance of modern macro, and my disagreements with modern macro.”