笨狼发牢骚

发发牢骚,解解闷,消消愁

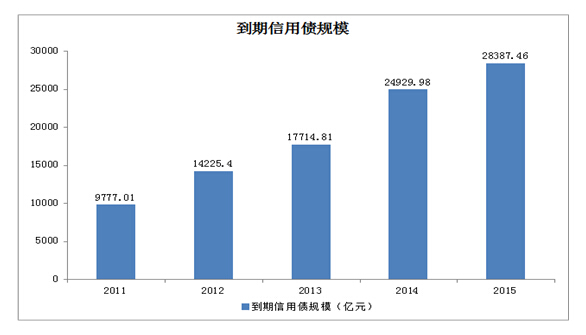

以前说起中国经济(比如克鲁格曼论债务,2015中国经济预测),都提到了中国的债务,这是一些与中国债务有关的图:

中国债务状况挺严重,没有什么快速的法子来解决,是个大问题。不过以此断言中国经济危机重重,甚至说2015年大灾难,理由还没有充分的。克鲁格曼论债务里就专门说债务用的恰当,不是坏事。

举个例子,如果你觉得今年中国不行了,你必须先解释为什么日本还没事儿,因为日本的债务比中国严重得多。下面的文章就说也许大家觉得日本没事儿,日本的问题没什么出路,难说不对世界经济带来灾难。

早些时候的一些观察:

2014.12.07安倍上台后在经济上的作为

2015.02.16日本2014全年总产值原地不前

财富杂志(Fortune):Forget Greece, Japan is the world's real economic time bomb(希腊小菜一碟,日本才是世界的隐患)

Chris Matthew

How Japan handles its government debt will have a bigger impact on the U.S. economy.

The eyes of the financial world are on the high drama playing out in Greece right now, and for good reason. Greece’s attempts to renegotiate its debt will redefine how the member nations of the world’s largest economy—the European Union—interact for years to come.

But at the end of the day, even if Greece is forced out of the euro, the wider effects will likely be manageable. If Greece were to suffer a banking crisis and severe recession, its economy isn’t that large (roughly the size of Louisiana’s), and European officials have done work to shore up the EU financial system so that it could withstand the shocks of a Grexit.

But there’s another economic drama unfolding nearly 10,000 kilometers away from the Mediterranean that will be far more consequential. The slowly unfolding fiscal crisis in Japan might not have the same entertainment value as the action in Athens. After all, what’s more riveting (and deliciously ironic) than watching the colorful and self-described Marxist Greek finance minister Yanis Varoufakis battle it out with the world’s most powerful woman, and former East German, Angela Merkel?

Nevertheless, the situation in Japan, the world’s third largest economy, will have a greater impact on the global economy in the years to come than Greece ever will. And for aging Western Democracies like the U.S., watching what unfolds in Japan may be like looking into a crystal ball of our own economic future.

Takatoshi Ito, an economist at Columbia’s School of International & Public Affairs, argued at a panel discussion on Monday that unless the Japanese government can raise its sales tax to north of 15%, from its current 8%, Japan’s economy will suffer a fiscal crisis sometime between 2021 and 2023. That’s because as Japan’s population continues to age, its famously high savings rate will have to fall, and the Japanese public will no longer be able to absorb the large amount of debt the government is assuming.

Unlike Greece, the Japanese government can print as many yen as it wants to pay its debts—debts that are largely owned by the government, Japanese banks, and citizens. So there’s no reason Japan would have to default on its debt. But all that money printing, argued Ito, will lead to an inflation crisis and a serious decline in the Japanese standard of living.

Ito’s co-panelist, Japan scholar Gerald Curtis, doesn’t believe that the Japanese government will raise the sales tax to 15% any time soon. Prime Minister Shinzo Abe’s decision to delay a sales tax increase from 8% to 10% until 2017 is indicative of the government’s inability to force such painful policies on the public. “It’s very hard for me to see how we get from here to there,” said Curtis. If Both Ito and Curtis are right, that means we’re just a few short years away from a fiscal crisis in Japan.

Others are not so sure. It’s been clear for two decades that Japan faces demographic difficulties. Its low birthrate and cultural aversion to immigration means that its working age population is shrinking at an alarming rate while the population of non-working retirees (who demand expensive healthcare) is on the rise. This dynamic has lead countless traders to bet against Japanese debt, with disastrous results, even though the demographic predictions that led traders to bet against the nation have come true.

So why hasn’t there been a fiscal crisis in Japan, and should we believe prognosticators like Ito, who continue to say it’s imminent? For economists like Paul Krugman, worrying over a possible inflation crisis in Japan seven years from now is crazy when you have a very real problem of stagnant growth and deflation right now.

At the same time, problems like chronic inflation, and deflation for that matter, can crop up unexpectedly and then be hard to thwart once they’ve reared their ugly heads. Sure, the developed world’s main problem today is deflation, but Ito’s point is that if you rely solely on the central bank to fund your debt for too long, people will look elsewhere to store their cash. One need only look to the U.S. economy in the 1960s and 1970s to see how quickly persistent inflation can turn into a serious economic problem. As economist Christina Romer points out in a 2007 paper, the inflation during that period was partly the result of policymakers’ overoptimistic assumptions about the U.S. economy.

It’s entirely reasonable, given the developed world’s slowing productivity growth and Japan’s shrinking population, that the economic growth we’re seeing is close to as good as it will get. Ito’s point, then, is that we should be wary of delaying the inevitable, simply raise taxes now, and admit that growth in Japan is just not going to be that great in the coming decade.

No matter what happens to Japan, the U.S. and Europe should pay close attention. Those economies must also contend with the issue of slow growth and an aging population. How much can government spending and central bank policy solve these problems? What happens in Japan over the next decade should give us a clear answer.