正文

Let's start with your question about supply and demand creating the housing bubble. We make the case in our Open Letter to Federal Reserve Chairman Ben S. Bernanke that the Fed's rate cuts caused the housing bubble:

Let's move on to your question about fictitious value. In the chart to the left from Groundhog day in the housing marketwe see the Case-Shiller home prices index plotted against a 3.3% meanUS inflation rate. The delta is the fictitious value created during thehousing bubble. Your question is whether the Case-Shiller numbers areinflation-adjusted and the answer is: yes. You additionally askquestion whether the CPI adjustment is itself valid or if itunderstates inflation.

John Williamsnotes at ShadowStats that the CPI has been reformulated so many timessince the Nixon administration that comparing the inflated price ofapples today to apples 20 years ago is impossible. It gets worse. Atleast we have Production/Consumption Economy inflation numbers to argueabout. Inflation measures for the FIRE Economy don't even exist, andreal estate has been the centerpiece of FIRE Economy policy since thepassage of the Tax Reform Act of 1986.

Monetary policy is separate and in fact the opposite for the FIREEconomy and P/C Economy, so it doesn't make sense to adjust FIREEconomy asset inflation, such as in housing, using P/C Economyinflation measures like the CPI. The CPI is only marginally better forthis purpose than using, say, annual inches of rainfall in WashingtonDC. By using the CPI what we are really measuring is the rise of theresidential real estate sub-sector of the FIRE Economy compared to aninflation measure, arguably itself dubious, of the P/C Economy.

Now we enter the house of mirrors, so to speak. What we reallywant to do is compare the Case-Shiller home price appreciation numbersto overall FIRE Economy inflation. Unfortunately, the BLS doesn't measure FIRE Economy employment, GDP, and inflation, so we have to guess at it.

One measure of FIRE Economy growth is the amount of debt created. In Economic Cognitive Dissonance we take a stab at it with this chart.

It shows the combined FIRE and P/C Economies doubling debt levelsbetween 1996 and 2006, from $14 trillion to $28 trillion. The debttaken on by the FIRE Economy grew more than 250% over the period, fromnearly $4 trillion to nearly $14 trillion. Total business debt, whichis mostly P/C Economy debt, grew by a modest 100%, from just over $2trillion to just over $4 trillion. One interpretation of this is thatreal estate merely kept up with the rate of overall FIRE Economyinflation, and that no fictitious value was created within the FIREEconomy, from a FIRE Economy-centric view.

Right about now your wondering if this hall of mirrors has an exit. No,it leads to the question, how much of the value in the entire FIREEconomy is fictitious? From the perspective of the P/C Economy, allFIRE Economy growth off the 100 year trend line of FIRE Economy growthsince 1980 can be considered fictitious. We'd hate to say how much thatis, but the $13 trillion we assign to real estate is likely anunderstatement.

Payments that occur within the FIRE Economy are only relevant to theP/C Economy when they either escape or are not captured. As Hudsonexplains in grueling detail, the tax law system is designed to makesure that profits earned within the FIRE Economy stay there. If you tryto take them out, the tax rate is so high that your profits arevirtually wiped out. But if you use your profits to buy more realestate or other FIRE Economy assets then the tax rate is low on thetransaction, as low as zero in some cases.

The FIRE Economy can implode if debts cannot be repaid out of profits within the FIRE Economy, due to asset pricedeflation or out of income from wages that the FIRE Economy captures aswhat economist's call "economic rent." This happened to Japan's FIREEconomy gradually since 1992 and the USA's suddenly after 1929. Thesystem of capturing wages as economic rent for the FIRE Economy brokedown. Asset price deflation was transmitted into the P/C Economy,leading to unemployment and declines in demand generally, which in turndepressed the FIRE Economy.

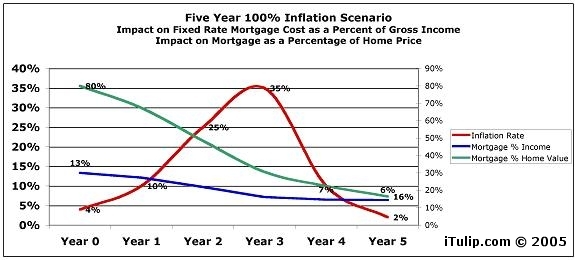

This leads us finally to your last question: can wageinflation be used to prevent a collapse in the real estate sector ofthe FIRE Economy? We explored this idea in Inflation is Dead! Long Live Inflation! It lays out a hypothetical 100% six year inflation and the impact on debt.

In our view, a period of high wage inflation can rescue the FIREEconomy. Granted, there are a lot of political reasons why thisscenario is unlikely since it represents what FIRE Economy interestsview as an unfortunate transfer of wealthin the wrong direction, from creditors to debtors. The preferredapproach that benefits the banks that back the FIRE Economy is to keepre-financing and extending existing debts, for example turning 30 yearmortgages into 50 or 100 year mortages. So that is likely what we willsee.

"Asthe Fed lowered short term interest rates from 6.5% May 2000 to 1% June2003, LIBOR which is used by banks to set the variable portion ofadjustable rate mortgages (ARM) declined to 1.25%. s a result, themonthly interest rate on an ARM declined from 6.5% to as low as 2.0%,effectively reducing the monthly cost of a $1,000,000 home in 2003 tothe cost of a $630,000 home purchased with a 6.5% ARM or fixed ratemortgage a few years before. Not surprisingly, an unusually largenumbers of ARMs were sold. Several years are needed for home buildersto gear up and build new homes to increase supply. However, interestrates were dropped quickly and so credit and the money supply rapidlyincreased. Home prices therefore rose quickly."

|

John Williamsnotes at ShadowStats that the CPI has been reformulated so many timessince the Nixon administration that comparing the inflated price ofapples today to apples 20 years ago is impossible. It gets worse. Atleast we have Production/Consumption Economy inflation numbers to argueabout. Inflation measures for the FIRE Economy don't even exist, andreal estate has been the centerpiece of FIRE Economy policy since thepassage of the Tax Reform Act of 1986.

Monetary policy is separate and in fact the opposite for the FIREEconomy and P/C Economy, so it doesn't make sense to adjust FIREEconomy asset inflation, such as in housing, using P/C Economyinflation measures like the CPI. The CPI is only marginally better forthis purpose than using, say, annual inches of rainfall in WashingtonDC. By using the CPI what we are really measuring is the rise of theresidential real estate sub-sector of the FIRE Economy compared to aninflation measure, arguably itself dubious, of the P/C Economy.

Now we enter the house of mirrors, so to speak. What we reallywant to do is compare the Case-Shiller home price appreciation numbersto overall FIRE Economy inflation. Unfortunately, the BLS doesn't measure FIRE Economy employment, GDP, and inflation, so we have to guess at it.

One measure of FIRE Economy growth is the amount of debt created. In Economic Cognitive Dissonance we take a stab at it with this chart.

It shows the combined FIRE and P/C Economies doubling debt levelsbetween 1996 and 2006, from $14 trillion to $28 trillion. The debttaken on by the FIRE Economy grew more than 250% over the period, fromnearly $4 trillion to nearly $14 trillion. Total business debt, whichis mostly P/C Economy debt, grew by a modest 100%, from just over $2trillion to just over $4 trillion. One interpretation of this is thatreal estate merely kept up with the rate of overall FIRE Economyinflation, and that no fictitious value was created within the FIREEconomy, from a FIRE Economy-centric view.

Right about now your wondering if this hall of mirrors has an exit. No,it leads to the question, how much of the value in the entire FIREEconomy is fictitious? From the perspective of the P/C Economy, allFIRE Economy growth off the 100 year trend line of FIRE Economy growthsince 1980 can be considered fictitious. We'd hate to say how much thatis, but the $13 trillion we assign to real estate is likely anunderstatement.

Payments that occur within the FIRE Economy are only relevant to theP/C Economy when they either escape or are not captured. As Hudsonexplains in grueling detail, the tax law system is designed to makesure that profits earned within the FIRE Economy stay there. If you tryto take them out, the tax rate is so high that your profits arevirtually wiped out. But if you use your profits to buy more realestate or other FIRE Economy assets then the tax rate is low on thetransaction, as low as zero in some cases.

The FIRE Economy can implode if debts cannot be repaid out of profits within the FIRE Economy, due to asset pricedeflation or out of income from wages that the FIRE Economy captures aswhat economist's call "economic rent." This happened to Japan's FIREEconomy gradually since 1992 and the USA's suddenly after 1929. Thesystem of capturing wages as economic rent for the FIRE Economy brokedown. Asset price deflation was transmitted into the P/C Economy,leading to unemployment and declines in demand generally, which in turndepressed the FIRE Economy.

|

In our view, a period of high wage inflation can rescue the FIREEconomy. Granted, there are a lot of political reasons why thisscenario is unlikely since it represents what FIRE Economy interestsview as an unfortunate transfer of wealthin the wrong direction, from creditors to debtors. The preferredapproach that benefits the banks that back the FIRE Economy is to keepre-financing and extending existing debts, for example turning 30 yearmortgages into 50 or 100 year mortages. So that is likely what we willsee.

评论

目前还没有任何评论

登录后才可评论.