正文

啥叫线性思维?就是把过去的经历画一条直线无限延伸到未来,可现实不是那么玩儿的,儿童时的宝贝会变成少年时的垃圾

过去三十年对美国社会最有影响的就是由联储会的一低再低的利率政策吹大的金融泡沫、债务泡沫,美国的房价只不过是其中的症状之一。如果俺赶上了那个好时机,那是俺的狗屎运,俺可不敢说俺有多聪明、自以为找到了财富的源泉,更没脸去教别人咋赚钱

要说运气,过去二、三十年跟上利率快车的可比房子通胀前的4%赚得多多了,那时俺银行CD的利息都超过10%,要是债券还要加上增值,更不必整天跟社会渣滓打交道

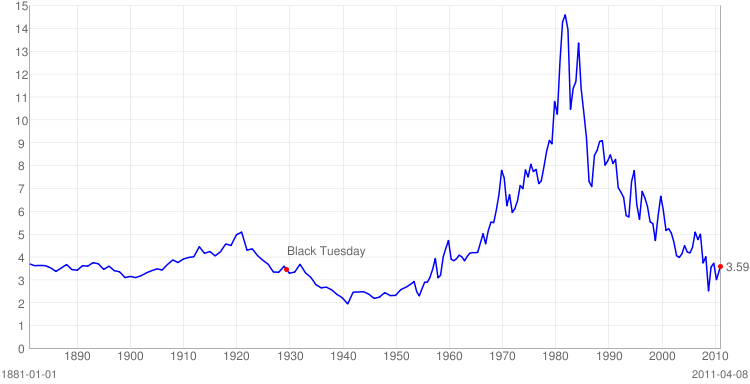

仔细瞧瞧十年利率吧,未来十几、二十年是该升还是该降?为啥2006年房市崩了?利率涨起来了呗,而且就涨了那么一点。连房价到底为嘛涨、为嘛跌都不了还搞啥房地产?

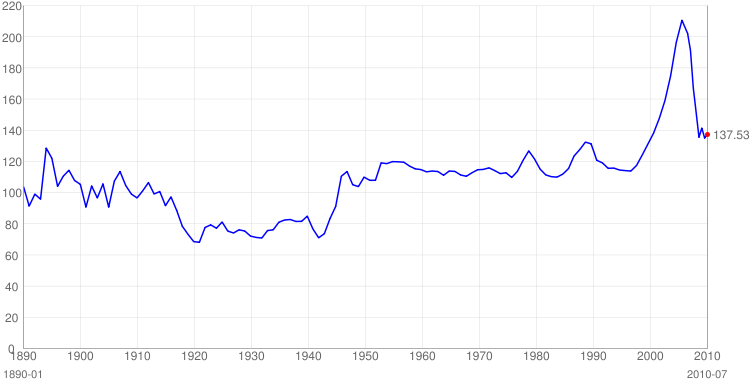

真实房价

Americans Shun Cheapest Homes in 40 Years as Owning Loses Appeal

bloomberg

By Kathleen M. Howley - Apr 18, 2011

The most affordable real estate in a generation is failing to lure buyers as Americans sour on the idea of home ownership. Photographer: Matthew Staver/Bloomberg

Victoria Pauli signed a one-year lease last week to stay in her rental home in Fair Oaks, California. She had considered buying in the area, where property prices have slumped 57 percent since a 2005 peak.

In the end, she decided it wasn’t worth it.

“I know people who have watched their home values get cut in half, and I know people who are losing their homes,” said Pauli, 31, who works as a property manager for a real estate company. “It’s part of the American dream to want to own your own home, and I used to feel that way, but now I tell myself: Be careful what you wish for.”

The most affordable real estate in a generation is failing to lure buyers as Americans like Pauli sour on the idea of home ownership. At the end of 2010, the fourth year of the housing collapse, the share of people who said a home was a safe investment dropped to 64 percent from 70 percent in the first quarter. The December figure was the lowest in a survey that goes back to 2003, when it was 83 percent.

“The magnitude of the housing crash caused permanent changes in the way some people view home ownership,” said Michael Lea, a finance professor at San Diego State University. “Even as the economy improves, there are some who will never buy a home because their confidence in real estate is gone.”

Worse Than Depression

Historically, homes have been a safer investment than equities. During 2008, the worst year of the housing crisis, the median U.S. home price declined 15 percent, compared with a more than 38 percent plunge in the Standard & Poor’s 500 Index.

Americans stay in their homes for a median of eight years, according to the National Association of Realtors in Chicago. Someone who bought a home in 2002 and sold in 2010 saw a 4.8 percent increase in value, based on the annualized median price measured by the group. The average annual gain in the past 20 years was 4.2 percent.

Falling prices have made real estate the best buy in at least four decades. Housing affordability reached a record in December, according to National Association of Realtors data that go back to 1970. The group bases its gauge on property prices, mortgage rates and the median U.S. income.

The median U.S. home price tumbled 32 percent from a 2006 peak to a nine-year low in February, data from the Realtors show. The retreat surpassed the 27 percent drop seen in the first five years of the Great Depression, according to Stan Humphries, chief economist of Zillow Inc., a Seattle-based real estate information company.

Not Risk-Free

“If we’ve learned anything from this mess, it’s that housing is not a risk-free investment,” said Michelle Meyer, a senior economist at Bank of America Merrill Lynch Global Research in New York. “Everyone knows someone underwater in their mortgage or struggling to sell a home.”

About 11 million U.S. homes were worth less than their mortgages at the end of 2010, according to CoreLogic Inc., a Santa Ana, California-based real estate information company. An additional 2.4 million borrowers had less than five percent equity, meaning they’ll be underwater with even slight price declines, according to the March 8 report. The two categories add up to 28 percent of residences with mortgages.

The share of Americans who said they plan to purchase a home in the next six months tumbled 23 percent in March, according to the Conference Board research firm in New York. The National Association of Realtors probably will say tomorrow that existing-home sales were at a 5 million annual rate in March, up 2.5 percent after a 9.6 percent plunge in February, according to the median estimate of 74 economists surveyed by Bloomberg.

Improving Employment

The drop in confidence may be temporary. Home sales probably will rise 4.1 percent to 5.1 million in 2011, with the biggest increases in the second half of the year, the Mortgage Bankers Association said in an April 14 report. In 2012, sales may climb 5.9 percent to 5.4 million, the highest pace since 2007, the Washington-based trade group estimated.

A rebound in home sales depends on the availability of jobs, the mortgage association said. The unemployment rate probably will decline every quarter of this year and next, falling to 7.9 percent by 2012’s end, the trade group said. It was 8.8 percent last month, the lowest in two years.

“We expect that purchase activity will pick up slowly as the improvement in the job market eventually leads to greater willingness to buy,” the mortgage bankers group said.

Low Mortgage Rates

Borrowing costs are at historic lows. The average U.S. rate for a 30-year fixed mortgage was 4.69 percent last year, the lowest in annual data going back to 1972, according to mortgage financier Freddie Mac, based in McLean, Virginia. The rate in March was 4.84 percent, the company said.

By 2012’s fourth quarter, the average fixed rate may rise to 6 percent, according to the Mortgage Bankers Association.

“If you can jump through the hoops to get a mortgage, and there will be hoops, then this is an amazing time to purchase real estate,” said Robert Stein, a senior economist at First Trust Portfolios LP in Wheaton, Illinois, and the former head of the Treasury Department’s Office of Economic Policy. “There are going to be a lot of people kicking themselves a few years from now because they didn’t take advantage of the low prices and the low mortgage rates.”

Cheap financing hasn’t done enough to boost home sales in part because lenders are being more selective with applicants, according to Federal Reserve Chairman Ben Bernanke. Fed policy makers have described the housing market as “depressed” in statements following their last eight meetings.

Tighter Lending

“Although mortgage rates are low and house prices have reached more affordable levels, many potential homebuyers are still finding mortgages difficult to obtain and remain concerned about possible further declines in home values,” Bernanke said in Congressional testimony last month.

The share of banks reporting tighter mortgage standards in the first quarter rose to 16 percent, the highest since 1991, according to the Fed’s Senior Loan Officer Survey.

Federal regulators are proposing rules that may make lending even more stringent, including a requirement that banks and bond issuers keep a stake in home loans they securitize if the mortgage borrowers have imperfect credit and down payments of less than 20 percent. Borrowers who don’t meet the criteria would pay higher rates to compensate lenders for risk.

As mortgage requirements rise, rates could follow as Congress and the Obama administration consider phasing out government-controlled Fannie Mae and Freddie Mac. The companies hold federal charters mandating they increase the availability of mortgages through securitization. In Fannie Mae’s case, that order goes back to the Great Depression, when it was created as part of President Franklin D. Roosevelt’s New Deal.

Unsettled Issues

“There are a lot of unsettled policy issues on the table right now that, if they’re not handled right, could further set back the housing market,” said Richard DeKaser, an economist at Parthenon Group in Boston. “Fannie and Freddie have historically lowered interest rates, and eliminating them will increase the cost of home ownership.”

The U.S. home ownership rate dropped to 66.5 percent in the fourth quarter, the lowest in more than a decade, according to the Census Department. The rate probably will retreat another percentage point by 2013, according to Meyer, of Bank of America Merrill Lynch, and Lea, the finance professor. That would put it back to a 1997 level.

“People will still aspire to own their own homes,” Lea said. “They’ll just be a lot more practical about it.”

Pauli, the California renter, said she has no such aspirations, at least for now. She pays $1,500 a month for her three-bedroom, single-family home with a two-car garage, granite kitchen countertops and stainless-steel appliances. Her neighbors who bought before the housing crash typically have mortgage payments of about $2,800 a month, Pauli said.

“I don’t see myself purchasing, even with all the great prices I see,” Pauli said. “Going to bed every night worrying about your home value doesn’t sound like a good time to me.”

http://www.bloomberg.com/news/2011-04-19/americans-shun-most-affordable-homes-in-generation-as-owning-loses-appeal.html

过去三十年对美国社会最有影响的就是由联储会的一低再低的利率政策吹大的金融泡沫、债务泡沫,美国的房价只不过是其中的症状之一。如果俺赶上了那个好时机,那是俺的狗屎运,俺可不敢说俺有多聪明、自以为找到了财富的源泉,更没脸去教别人咋赚钱

要说运气,过去二、三十年跟上利率快车的可比房子通胀前的4%赚得多多了,那时俺银行CD的利息都超过10%,要是债券还要加上增值,更不必整天跟社会渣滓打交道

仔细瞧瞧十年利率吧,未来十几、二十年是该升还是该降?为啥2006年房市崩了?利率涨起来了呗,而且就涨了那么一点。连房价到底为嘛涨、为嘛跌都不了还搞啥房地产?

真实房价

Americans Shun Cheapest Homes in 40 Years as Owning Loses Appeal

bloomberg

By Kathleen M. Howley - Apr 18, 2011

The most affordable real estate in a generation is failing to lure buyers as Americans sour on the idea of home ownership. Photographer: Matthew Staver/Bloomberg

Victoria Pauli signed a one-year lease last week to stay in her rental home in Fair Oaks, California. She had considered buying in the area, where property prices have slumped 57 percent since a 2005 peak.

In the end, she decided it wasn’t worth it.

“I know people who have watched their home values get cut in half, and I know people who are losing their homes,” said Pauli, 31, who works as a property manager for a real estate company. “It’s part of the American dream to want to own your own home, and I used to feel that way, but now I tell myself: Be careful what you wish for.”

The most affordable real estate in a generation is failing to lure buyers as Americans like Pauli sour on the idea of home ownership. At the end of 2010, the fourth year of the housing collapse, the share of people who said a home was a safe investment dropped to 64 percent from 70 percent in the first quarter. The December figure was the lowest in a survey that goes back to 2003, when it was 83 percent.

“The magnitude of the housing crash caused permanent changes in the way some people view home ownership,” said Michael Lea, a finance professor at San Diego State University. “Even as the economy improves, there are some who will never buy a home because their confidence in real estate is gone.”

Worse Than Depression

Historically, homes have been a safer investment than equities. During 2008, the worst year of the housing crisis, the median U.S. home price declined 15 percent, compared with a more than 38 percent plunge in the Standard & Poor’s 500 Index.

Americans stay in their homes for a median of eight years, according to the National Association of Realtors in Chicago. Someone who bought a home in 2002 and sold in 2010 saw a 4.8 percent increase in value, based on the annualized median price measured by the group. The average annual gain in the past 20 years was 4.2 percent.

Falling prices have made real estate the best buy in at least four decades. Housing affordability reached a record in December, according to National Association of Realtors data that go back to 1970. The group bases its gauge on property prices, mortgage rates and the median U.S. income.

The median U.S. home price tumbled 32 percent from a 2006 peak to a nine-year low in February, data from the Realtors show. The retreat surpassed the 27 percent drop seen in the first five years of the Great Depression, according to Stan Humphries, chief economist of Zillow Inc., a Seattle-based real estate information company.

Not Risk-Free

“If we’ve learned anything from this mess, it’s that housing is not a risk-free investment,” said Michelle Meyer, a senior economist at Bank of America Merrill Lynch Global Research in New York. “Everyone knows someone underwater in their mortgage or struggling to sell a home.”

About 11 million U.S. homes were worth less than their mortgages at the end of 2010, according to CoreLogic Inc., a Santa Ana, California-based real estate information company. An additional 2.4 million borrowers had less than five percent equity, meaning they’ll be underwater with even slight price declines, according to the March 8 report. The two categories add up to 28 percent of residences with mortgages.

The share of Americans who said they plan to purchase a home in the next six months tumbled 23 percent in March, according to the Conference Board research firm in New York. The National Association of Realtors probably will say tomorrow that existing-home sales were at a 5 million annual rate in March, up 2.5 percent after a 9.6 percent plunge in February, according to the median estimate of 74 economists surveyed by Bloomberg.

Improving Employment

The drop in confidence may be temporary. Home sales probably will rise 4.1 percent to 5.1 million in 2011, with the biggest increases in the second half of the year, the Mortgage Bankers Association said in an April 14 report. In 2012, sales may climb 5.9 percent to 5.4 million, the highest pace since 2007, the Washington-based trade group estimated.

A rebound in home sales depends on the availability of jobs, the mortgage association said. The unemployment rate probably will decline every quarter of this year and next, falling to 7.9 percent by 2012’s end, the trade group said. It was 8.8 percent last month, the lowest in two years.

“We expect that purchase activity will pick up slowly as the improvement in the job market eventually leads to greater willingness to buy,” the mortgage bankers group said.

Low Mortgage Rates

Borrowing costs are at historic lows. The average U.S. rate for a 30-year fixed mortgage was 4.69 percent last year, the lowest in annual data going back to 1972, according to mortgage financier Freddie Mac, based in McLean, Virginia. The rate in March was 4.84 percent, the company said.

By 2012’s fourth quarter, the average fixed rate may rise to 6 percent, according to the Mortgage Bankers Association.

“If you can jump through the hoops to get a mortgage, and there will be hoops, then this is an amazing time to purchase real estate,” said Robert Stein, a senior economist at First Trust Portfolios LP in Wheaton, Illinois, and the former head of the Treasury Department’s Office of Economic Policy. “There are going to be a lot of people kicking themselves a few years from now because they didn’t take advantage of the low prices and the low mortgage rates.”

Cheap financing hasn’t done enough to boost home sales in part because lenders are being more selective with applicants, according to Federal Reserve Chairman Ben Bernanke. Fed policy makers have described the housing market as “depressed” in statements following their last eight meetings.

Tighter Lending

“Although mortgage rates are low and house prices have reached more affordable levels, many potential homebuyers are still finding mortgages difficult to obtain and remain concerned about possible further declines in home values,” Bernanke said in Congressional testimony last month.

The share of banks reporting tighter mortgage standards in the first quarter rose to 16 percent, the highest since 1991, according to the Fed’s Senior Loan Officer Survey.

Federal regulators are proposing rules that may make lending even more stringent, including a requirement that banks and bond issuers keep a stake in home loans they securitize if the mortgage borrowers have imperfect credit and down payments of less than 20 percent. Borrowers who don’t meet the criteria would pay higher rates to compensate lenders for risk.

As mortgage requirements rise, rates could follow as Congress and the Obama administration consider phasing out government-controlled Fannie Mae and Freddie Mac. The companies hold federal charters mandating they increase the availability of mortgages through securitization. In Fannie Mae’s case, that order goes back to the Great Depression, when it was created as part of President Franklin D. Roosevelt’s New Deal.

Unsettled Issues

“There are a lot of unsettled policy issues on the table right now that, if they’re not handled right, could further set back the housing market,” said Richard DeKaser, an economist at Parthenon Group in Boston. “Fannie and Freddie have historically lowered interest rates, and eliminating them will increase the cost of home ownership.”

The U.S. home ownership rate dropped to 66.5 percent in the fourth quarter, the lowest in more than a decade, according to the Census Department. The rate probably will retreat another percentage point by 2013, according to Meyer, of Bank of America Merrill Lynch, and Lea, the finance professor. That would put it back to a 1997 level.

“People will still aspire to own their own homes,” Lea said. “They’ll just be a lot more practical about it.”

Pauli, the California renter, said she has no such aspirations, at least for now. She pays $1,500 a month for her three-bedroom, single-family home with a two-car garage, granite kitchen countertops and stainless-steel appliances. Her neighbors who bought before the housing crash typically have mortgage payments of about $2,800 a month, Pauli said.

“I don’t see myself purchasing, even with all the great prices I see,” Pauli said. “Going to bed every night worrying about your home value doesn’t sound like a good time to me.”

http://www.bloomberg.com/news/2011-04-19/americans-shun-most-affordable-homes-in-generation-as-owning-loses-appeal.html

评论

目前还没有任何评论

登录后才可评论.