"Investors should remember that excitement and expenses are their enemies. And if they insist on trying to time their participation in equities, they should try to be fearful when others are greedy and greedy when others are fearful." - Warren Buffett

Greed and Fear.

One of the fascinating things about markets is how quickly investors can shift from one emotion to the other.

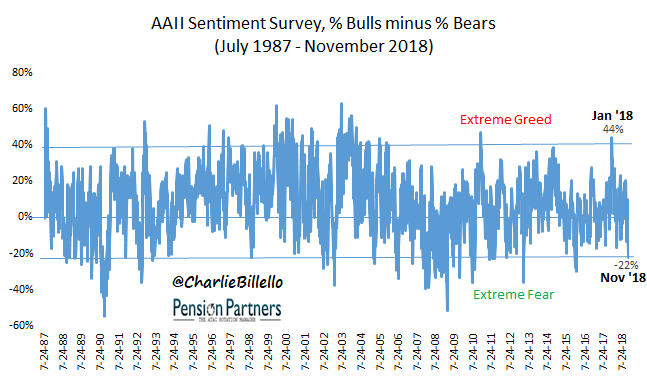

At the start of the year, investors were unequivocally greedy. And who could blame them? The S&P 500 had just completed its 9th straight up year and it did so without a pullback greater than 3%. In the AAII Sentiment Poll, Bulls outnumbered Bears by 44%. This was in the top 5% of all readings dating back to 1987.

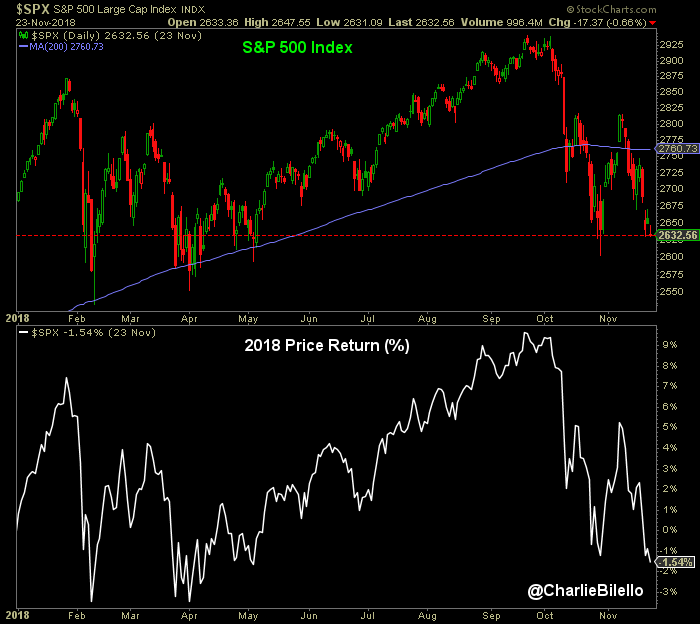

Fast forward to today and sentiment has shifted 180 degrees. Volatility has increased as the S&P 500 has experienced a pair of 10% corrections. In the same AAII Poll, Bears now outnumber Bulls by 22%, which is in the bottom 5% of all readings. Investors are now fearful.

Data Source for all charts/tables herein: AAII

What does this mean when it comes to markets?

As I indicated back in early January, extreme greed tends to be followed by below-average forward returns. Not in all cases, but more often than not.

That's indeed what we have seen since the start of the year, with the S&P 500 down 1.5%.

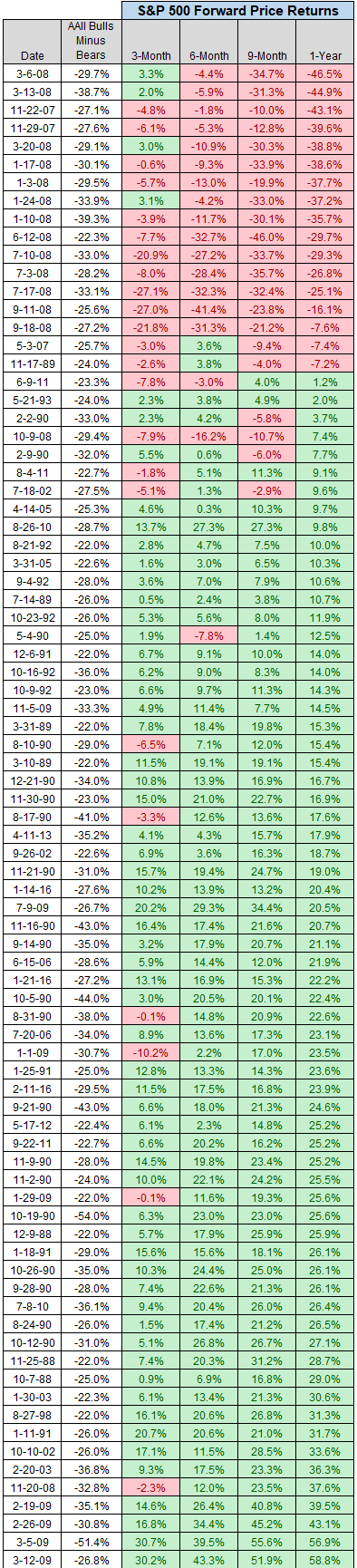

But today, with extreme fear in place, the opposite tendency is observable. When investors are fearful, forward returns tend to improve, with above-average outcomes over the subsequent year.

Does that always happen? No, there's no such thing as always in markets. In late 2007 and throughout 2008, bearish sentiment extremes were hit while the market continued lower. But the more common outcome has been higher prices a year later, as we have seen time and again since the equity market bottomed in 2009 (most recently in Jan/Feb 2016).

Table: Bottom 5% of AAII Bulls-Bears Readings and S&P 500 Forward Price Returns

What will happen today?

The best we can say based on the historical record is that forward returns are significantly better following extreme fear than extreme greed. Put simply: the odds favor a bounce.

The caveat: If we are in a juncture similar to late 2007, all bets are off. Under that scenario, we would see much more fear and lower prices before a sustainable rally took hold.